The idea of digital currency in India has made a very big step with the introduction of Central Bank Digital Currency (CBDC) provided by the Reserve Bank of India (RBI). It is one of the contemporary types of money involving a combination of both the comfort of online payments and the reliability and support of the government.

What is CBDC?

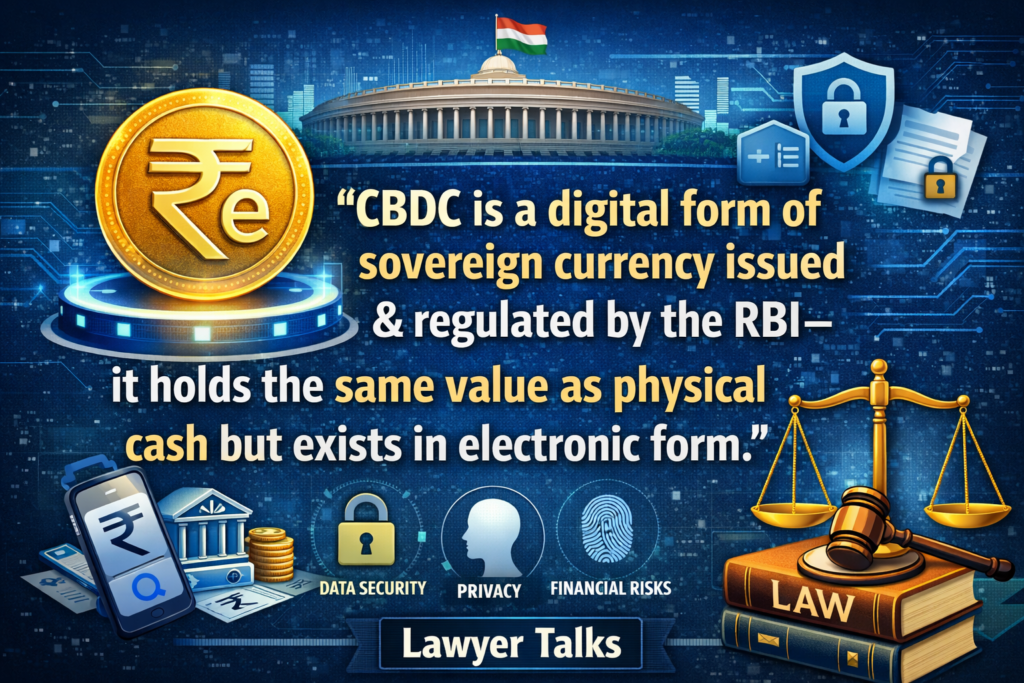

CBDC is merely the digital form of Indian currency of the RBI. It is equal to the physical cash though in an electronic format. Also, it is official, regulated and can be considered legal money contrary to cryptocurrencies.

India has presented two types of CBDC:

- The general population type of retail CBDC (e₹-R) would be usable.

- Banks and large financial institutions Wholesale CBDC (e₹-W)

Why is RBI Introducing CBDC?

RBI is focusing on the modernization of the financial system in India using CBDC. It assists in cutting down on the use of cash besides making transactions quicker and safer. It also facilitates financial inclusion through the easier access to digital payments.

The other important goal is to provide a secure alternative to privately issued cryptocurrencies, which are not always stable and regulated. CBDC gives the state monetary policy and circulation as well.

Legal Framework in India

CBDC is not functioning in a law-free space. It is based on the framework of the existing statutes, such as:

- Reserved bank of India Act, 1934 that has undergone some modifications to permit the issuance of digital currency.

- Digital transactions are organized by the Payment and Settlement Systems Act of 2007.

- RBI regulations and pilot project regulations.

CBDDC will be considered a legally binding currency after all being issued by the RBI, unlike other cryptocurrencies that do not have a clear standing on laws in India.

Major Legal Problems and Concerns.

Although there is good support of CBDC, some legal hurdles still persist.

Privacy Concerns:

Digital transactions can be traceable, which places the issue of monitoring finances and personal privacy in question.

Data Protection:

The sensitive financial information should be secured under certain frameworks such as the Digital Personal Data Protection Act, 2023.

Cybersecurity Risks:

CBDC being a digital system will also become exposed to cyber threats and will need high-level technological protection.

Impact on Banking System:

When individuals switch to CBDF in large numbers, there will be less deposits in conventional banks, which will influence their operations.

CBDC vs Cryptocurrency

CBDDC is completely opposed to cryptocurrencies. It is governed and issued by the RBI and therefore is stable and legally binding. On the contrary, cryptocurrencies are privately developed, transient, and not legally recognized in India.

Conclusion

CBDC introduction is a significant change in the sphere of finance and legal tightening in India. It is a mixture of innovativeness and regulation, providing a safe and state-supported digital payment system.

Nevertheless, whether it has been successful in the long run will deem upon its ability to solve problems such as privacy, data security and cybersecurity. CBDC is a dynamic field of law study and practice to lawyers and law students that law and technology cross with finance, which is very much pertinent in the digital age.

– Team Lawyer Talks